Retirement Math

When I retired, the first thing I did was search on the web for a formula that would

- tell me how much I could withdraw from my retirement accounts, such that

- each year, I want the withdrawal to be larger to keep up with inflation,

- assuming that the inflation rate and my accounts’ yield rate are constant.

After a bunch of fruitless searching, I decided to derive the equation myself. Here it is: \[ P_n = P_0 y^n - W y^n \left( \frac{1 - \left(\frac{i}{y}\right)^n}{1 - \frac{i}{y}}\right) \tag{1} \]

where

\(P_n\) is the \(n\text{th}\) year’s principal at year \(n\),

\(P_0\) is the initial principal at time 0,

\(W\) is the initial withdrawal which grows to keep up with inflation,

\(y\) is the yield ratio (e.g., 1.09 (9%)), and

\(i\) is the inflation ratio (e.g., 1.0325 (3.25%)).

Turns out this is called the formula for a Growth Annuity.

Derivation

Here’s the derivation:

\[ P_1 = (P_0 - W)y \] \[ P_2 = (P_1 - Wi)y \] \[ P_3 = (P_2 - Wi^2)y \] \[ etc. \]

Substituting the first equation into the second gives \[ P_2 = ((P_0 - W)y - Wi)y \]

and then simplifying yields \[ P_2 = P_0y^2 -Wy(y+i). \]

Substituting this into the third equation above gives \[ P_3 = (P_0y^2 - Wy(y+i) - Wi^2)y \]

which simplifies to \[ P_3 = P_0y^3 - Wy(y^2 + iy + i^2). \]

After a few more rounds, the general pattern becomes obvious \[ P_n = P_0y^n - Wy(y^{n-1} + y^{n-2} i + \cdots + y^{1} i^{n-2} + i^{n-1}). \]

The part inside the parentheses is a geometric series and, if \(\lvert i/y \rvert < 1\) (i.e., that inflation is less than the yield), can be written

\[ P_n = P_0 y^n - W y \left( \frac{1 - \left(\frac{i}{y}\right)^n}{1 - \frac{i}{y}}\, y^{n-1} \right) \] or \[ P_n = P_0 y^n - W y^n \left( \frac{1 - \left(\frac{i}{y}\right)^n}{1 - \frac{i}{y}}\right) \tag{1} \]

(And yes, I know I can factor out a \(y^n\).)

Uses

Now, using equation (1), we can calculate when we’ll run out of money, for given yield and inflation rates and a withdrawal that keeps up with inflation.

Setting \(P_n=0\) and solving for \(n\), yields \[ n = \frac{\ln\left( 1 - \displaystyle\frac{p_0}{w}\,(1 - i/y) \right)}{\ln\left(\frac{i}{y}\right)} \]

So, for example, if we want to live off of $100,000 per year and have $1,000,000, and we assume that the rate of inflation is 3.25% and that the yield of the S&P 500 will average out to 9%, then \[ n = \frac{\ln\left( 1 - \displaystyle\frac{1000000}{100000}\,(1 - 1.0325/1.09) \right)}{\ln\left(\frac{1.0325}{1.09}\right)} \]

or n = 13.8 years.

Alternatively, we might want to know how much we can withdraw so that the balance never reaches 0. Setting n to infinity and noting that the denominator is negative (since the inflation rate is less than the yield rate), we have:

\[ -∞= \ln\left( 1 - \displaystyle\frac{p_0}{w}\,(1 - i/y) \right) \]

So, \[ 0 = 1 - P_0/W (1- i/y) \]

Or, \[ W= P_0 (1- i/y) \]

Using our example numbers above shows that we can withdraw up to $52,752.29 (inflation-adjusted) per year and we’ll never run out of money.

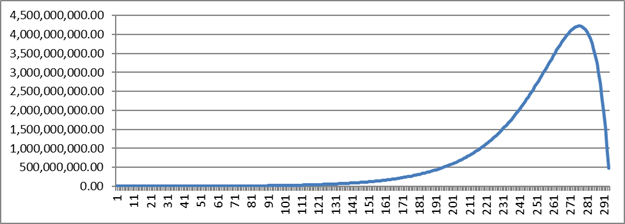

If we were to withdraw just one penny (inflation-adjusted) more every year, we’d have a financial meltdown several hundred years out:

I guess I’m not too worried about it.

Final Thoughts

So there are a couple of things wrong with my formula: it assumes that inflation and yield are constants, which is sort of ok in the very long run, but potentially terrible in the short-term. For example, you could run into sequence-of-returns risk. This is when you have a bunch of really bad years early in retirement, which could wipe you out.

And that’s why Bill Bengen, inventor of the 4% rule, ended up with less than my number (5.275%), because his is safer, a lot safer.

Another problem: suppose you have a bear year with a negative return, but a positive rate of inflation; or even if the rate of inflation is exactly equal to the yield. In these cases, the formula gives no guidance. Still my thinking is that so long as I withdraw significantly less than 5.275%, I’ll probably be ok.